The Fertilizer Situaion As we know it

The Fertilizer Squeeze of 2026: Why Prices are Spiking and How U.S. Farmers are Pivoting

As the 2026 spring planting season kicks into high gear, American agriculture is facing a tipping point. A major geopolitical conflict in the Middle East has sent fertilizer prices soaring forcing farmers, distributors, and the federal government to rethink how we feed our crops.

1. The Crisis at the Strait of Hormuz

The current shortage originates thousands of miles away, stemming from restrictions placed on the Strait of Hormuz since the Iran conflict began on February 28, 2026. This narrow waterway is critical, handling almost 30% of global fertilizer shipments and a substantial portion of the world's liquefied natural gas.

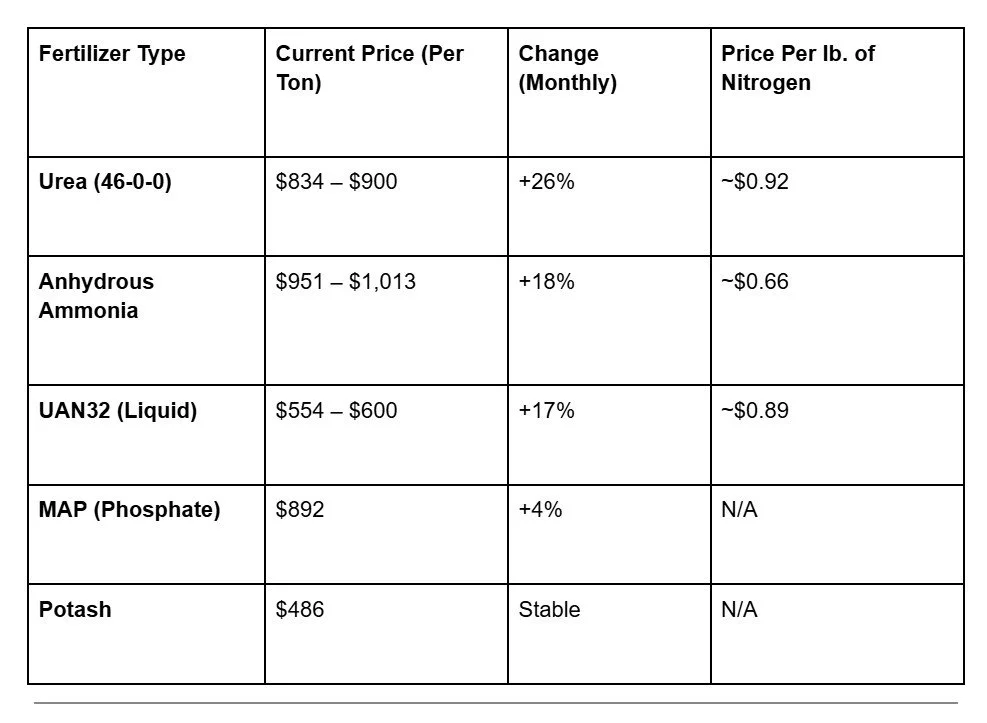

The Nitrogen Spike: Urea prices have skyrocketed roughly 26% in just the last month, averaging around $847 per ton.

The Logistics Stall: Shipments of urea and ammonia from the Persian Gulf have dropped significantly, leaving U.S. ports waiting for delayed vessels and forcing a scramble for alternative supply lines.

2. Current Market Prices (Retail Average – April 2026)

The following prices represent the sharp "post-conflict" spike. Nitrogen products, which rely heavily on natural gas and international shipping, are seeing the most aggressive jumps.

Current fertilizer prices and price changes

3. The "Rollins Plan": Reshoring and Relief

In response to these record highs, Agriculture Secretary Brooke Rollins has outlined an aggressive strategy to insulate American farmers from global volatility. Her plan focuses on "geographical immunity" and domestic strength:

Subsidizing Domestic Production: Rollins has suggested tapping into billions of dollars in tariff revenues to build new U.S.-based fertilizer infrastructure. "We must reshore our nutrient supply chain," she noted, aiming to reduce long-term reliance on the Middle East.

Import Diversification: To bridge the immediate gap, the USDA is looking toward the Western Hemisphere—specifically increasing imports from Venezuela and Canada—to avoid the risks associated with the Strait of Hormuz.

Challenging Market Concentration: Rollins has held high-level discussions with the "Big Four" fertilizer CEOs to address price stickiness and ensure that farmers aren't being squeezed by market consolidation during a global crisis.

4. The Shift to "Homegrown" Alternatives

With traditional synthetics at record prices, many growers are pivoting to biological and local substitutes that are entirely immune to international shipping disruptions:

Biological Nitrogen: Products like gene-edited microbes that are manufactured in U.S. labs that allow crops to "fix" their own nitrogen from the air, often some savings compared to current urea rates.

The Manure "Gold Rush": Livestock waste has become a hot commodity. Large-scale poultry and dairy operations are now major nutrient hubs for nitrogen and phosphorus.

Cover Crops: Many growers are leaning on "green manure" (clover, vetch) to bank nitrogen in the soil naturally for the 2027 season.

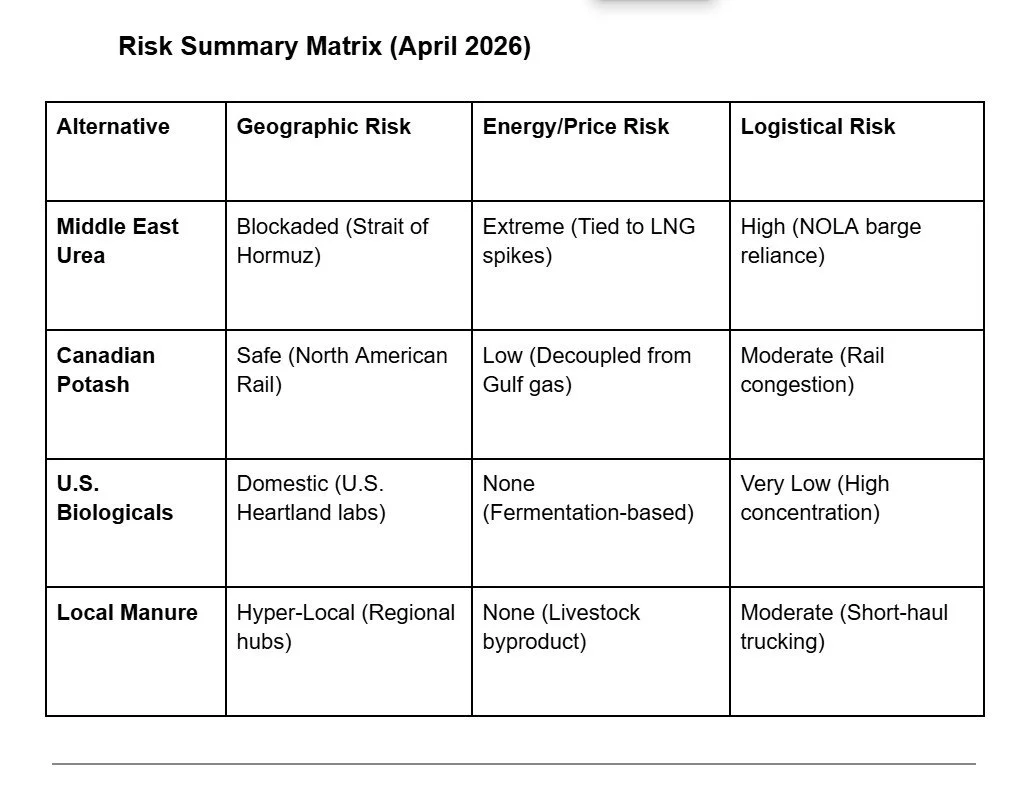

Fertilizer risk matrix

The Illinois Production Cost Report is the proxy used to help determine national price averages.

https://www.ams.usda.gov/mnreports/ams_3195.pdf

Read more articles here:

https://www.ifpri.org/blog/the-iran-wars-impacts-on-global-fertilizer-markets-and-food-production/