Corn at two year highs - here’s how we’re looking at it

Corn Isn't Trading Fundamentals Right Now

The current balance sheet doesn't justify $5 corn on paper. Stocks-to-use ratios historically require tightening to around 10% before prices sustain a meaningful move above that level. We're not there yet.

But this rally isn't a fundamentals story — it's a money flow story. Managed money just recorded their 4th largest weekly buying spree ever, now holding over 200,000 net long contracts. The record is around 400,000, which means there's still room to run if the narrative holds.

"Corn is a fuel play. With crude oil, war headlines, and fertilizer prices elevated, the funds are betting corn follows."

Ethanol accounts for 34% of all U.S. corn demand — roughly 5.6 billion bushels out of 16.47 billion in total use. So if crude stays above $90–$100, there's a logical argument that corn should follow higher. Every prior crude oil surge at these levels eventually pulled grains up with it.

Why We're Acting Now

Two-Year Highs Are a Reason to Do Something

December corn is right back near the highs from a prior Sunday night spike, approaching the $4.97 target — the 78.6% retracement of contract highs — with the contract high at $5.12 as the next level above that.

The daily chart is also showing bearish RSI divergence: prices are making new highs while momentum is not. That's a classic sign of a market losing energy. Last year you never got a chance to act at these levels. In 2024, this was the peak.

The goal isn't to sell everything — it's to do something. Whether that's locking in a floor, taking chips off the table, or adding downside protection on a portion of unpriced bushels.

One Trade To Look At

Taking advantage of high volatility - Sell 1 Dec $5.70 call - Sell 1 Dec 4.50 put - collect 35-40 cents

Collect approximately 35-40 cents of option premium and look for the volatility to decrease over time

How a Short Strangle Works

A short strangle is an options strategy where you simultaneously sell an out-of-the-money call and an out-of-the-money put on the same futures contract and expiration. You collect premium from both sides upfront — and as long as prices stay within a defined range, you keep it all.

Think of it like acting as the insurance company. Option buyers pay you a premium for price protection. In exchange, you take on the obligation to perform if prices move far enough in either direction. The wider the range stays, the more you profit.

📉 The Put You Sold ($4.50)

Gives the buyer the right to sell corn at $4.50. You collected 18¢ for taking that obligation. If corn stays above $4.50 at expiration, the put expires worthless and you keep the full 15¢.

📈 The Call You Sold ($5.70)

Gives the buyer the right to buy corn at $5.70. You collected 20¢ for taking that obligation. If corn stays below $5.70 at expiration, the call expires worthless and you keep the full 20¢.

Why Sell Implied Volatility Right Now?

Options are priced using implied volatility (IV) — essentially the market's expectation of how wildly prices will swing before expiration. Right now, with war headlines, crude oil swings, and the March 31st USDA report on the horizon, IV is elevated. That means options premiums are juicy.

When IV is high, selling options is attractive because you're collecting more premium than you would in a calm market. If volatility cools after the headlines settle — even if prices don't move much — the options you sold lose value faster. That decay is your profit.

We like selling the high implied volatility as a way to enhance your bottom line.

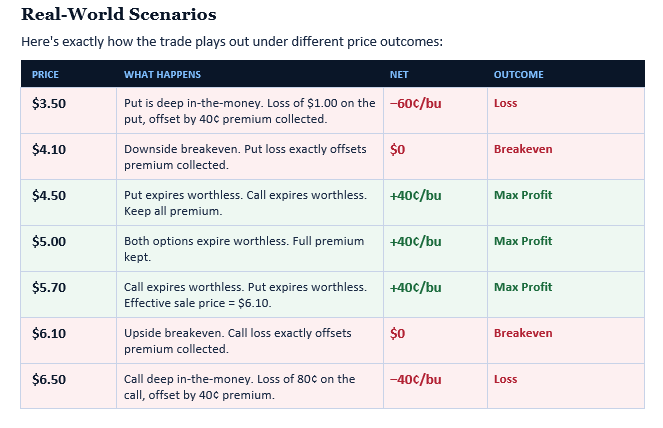

Level by level breakdown of strategy performance

You're Getting Paid to Be Patient

If you have unpriced bushels in the bin or new crop in the field, this trade lets you collect 38–40¢ per bushel today — while keeping your corn unpriced and waiting to see how the market develops. If corn stays between $4.50 and $5.70 by December expiration, you pocket the full premium. Think of it as adding 40 cents to whatever price you ultimately sell your corn for.

If corn runs past $5.70, you've given up some upside — but you're still receiving $6.10 effective before the call costs you anything. If corn crashes below $4.10, the put starts working against you, but you still have a partial floor near $4.50 on that portion of bushels.

This is not a substitute for a full marketing plan. It works best as a complement — layered on top of existing sales, hedges, or stored grain as a way to add cents to your average.

This Trade Is Not Without Downside

A short strangle is a powerful tool, but it comes with real obligations. Unlike buying options — where your max loss is the premium paid — selling options means your potential losses grow if the market makes a large sustained move in either direction.

• Margin risk: Selling options requires margin collateral. If the market moves sharply against you, you may face margin calls requiring additional funds on short notice. The margin on this position is $815 per contract.

• Unlimited upside risk: If December corn surges well past $6.10 — say a major supply shock — the short call can result in significant losses with no hard ceiling.

• Extended downside risk: If corn collapses below $4.10 due to a war resolution or bearish USDA report, the short put incurs mounting losses.

• Volatility spike risk: Even if prices don't move far, a surge in implied volatility can cause the options you sold to increase in value temporarily, creating paper losses before expiration.

• Not for everyone: This strategy requires understanding of options mechanics, margin management, and a clear overall marketing plan for your operation.